You can get a real edge over the competition when searching for foreclosure homes for flipping houses. In this post, I am going to show you the ways I was able to get houses even over the biggest home flippers in the industry.

The 2026 Edge: Why the Listing Agent Strategy Still Works

Hint: The edge has nothing to do with using a relative or friend that is a Realtor. It’s about understanding how the “Dual-Agent” dynamic can work in your favor when speed and numbers are everything.

Understanding the Modern Real Estate Landscape

As of 2026, the way agents are compensated has changed, but the roles remain distinct. There are two primary types of agents you’ll deal with: the Listing Agent, who represents the seller’s interests, and the Buyer’s Agent, who assists you in locating properties and navigating the sales process.

A major part of succeeding in this new landscape is knowing the property’s true value before you even call the agent. I recommend using a professional Home Value Estimator to identify equity gaps before other flippers even see the listing.

Leveraging the Listing Agent

A listing agent may list a property for a seller and also represent a buyer for that same property. When this happens, the Realtor is known as a Dual Agent. In Illinois, this requires written consent from both parties. While commissions are now more transparent and negotiable than they were in the past, the “leverage” for flipping houses remains the same:

By going directly to the listing agent, you simplify the communication chain. The listing agent becomes the “sole bridge” to the seller. When a listing agent can facilitate both sides of a transaction, they often have a much higher incentive to see your offer reach the finish line.

Typically when a listing (sellers) agent receives a commission from both sides of the deal, it ranges from 5-7 %, but there is no standard rate. On the other hand, when a buyers agent brings the buyer to the table, the commission is split between the two realtors, selling agent and buyers agent. This percentage is often 2.5 to 3.5 per agent.

Why Use A Listing Agent Opposed To A Buyers Agent For A Foreclosure?

A listing agent is working directly with the lender selling the property. In many cases the lender has developed a strong business relationship with the agent. The lender has a comfort level dealing one on one with the listing agent they hired. If they can eliminate the hassle of a third party they will.

Cutting Out The Middleman

Eliminating the middleman makes the transaction run more smoothly in the transaction. Although this may be good for the lender and the listing agent, as a broker myself, I do know there are pros and cons to this method. Let’s take a look at a few of the cons below.

- CON: The listing agent is the client of the lender so they are biased.

- CON: The listing agent may not have your best interest in mind. Again, they work for the lender.

- CON: Eliminates commission from another agent. You don’t spread the wealth to a family or friend agent.

Furthermore, the listing agent will work hard for you. They would love to assume the dual-agent status and receive commission from both sides of the deal.

In many instances a listing agent will discount their commission rate. Just ask prior to writing a contract with them! For example, say to the agent delicately, “I am interested in using you as my agent. Would you be willing to decrease your commission since I will be giving you dual-agent status?”

Remember allowing this to take place does not actually save you money on the purchase price. However, it does allow the lender to pay a lower commission rate – which gives you leverage.

The listing realtor is also making a far better commission because you found them and are allowing them to become the dual-agent. Therefore, do not feel awkward presenting this question! When an agent does not have to work at finding a client and the client finds them, it is a blessing.

Let’s look at a few examples of how we will benefit as investors from receiving a decrease in commission.

Commission Example Demonstrating How You Get More Deals

Assume that a lender received a contract at $100,000 on a property. Also, assume that a lender will pay a 6% commission rate. A 3% or $3000.00 commission would go to the listing agent and 3% or $3000.00 commission to the selling agent.

If a listing agent becomes a “dual agent” and cuts their commission to 4% vs. 6%, that is a $2000.00 savings to the lender.

1) Example 1- you put in a contract with a listing agent on a property listed for $100,000. You submit a contract for just under list price or $99,000. The listing agent has agreed to accept a 4% commission. Equal to $3,960.00

2) Example 2 – the competitor puts in a contract using an outside agent or buyers agent on the same $100,000 property. They have a stronger contract coming in at list price or $100,000. The commission total is 6% or 3% each agent. Equal to $6,000.00

Which contract would you presume is more favorable for the lender? Absolutely, Example 1 would allow for the lender to save $1040.00.

This is due to the commission difference from 6% – 4%. Although the contract of $100,000 was higher than yours by $1,000.00, the $2040.00 commission savings further offset the transaction.

This amount may not appear to be significant. However, the amount difference coupled with not dealing with outside agents, can make all the difference.

In many cases, listing realtors agree on less of a percentage than stated above. For example, a listing agent taking only one side of the commission at 2.5 – 3.5% is not uncommon.

Find Foreclosures to Flip & Get An Edge On The Bidding Process

You can locate listing agents by driving or farming the desired marketing area in which you are seeking. Online services such as Zillow is an additional resource for finding the listing agent directly. When you come across a new for sale sign while in hot pursuit of a property, call the listing realtor on the sign for the details.

After you view the interior and exterior of the property of interest and all of your due diligence is completed, submitting a contract for purchase is your next step!

How Much to Bid & When to Bid Over List Price?

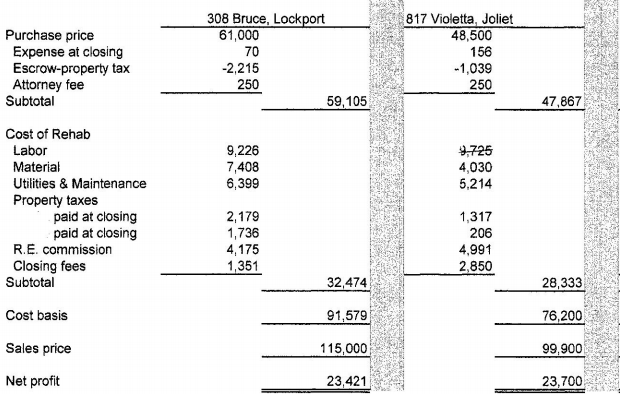

This is an important aspect of acquiring a foreclosure. Here is an example…

A property is listed for $70,000. Closing costs when you buy would be estimated at approximately $2,000. Repair costs are estimated at $12,000. When you sell, your estimated real estate commissions and closing costs are estimated at $6,000. This brings your total expenses to $20,000.

On this scenario, if you bid $65,000 for the property and get it, you would be in the property for $85,000.

Based on comparable property sales in the area, an after repaired value of the property would be $115,000. This will give you a potential profit of $30,000.

While working with your agent on the bid, you are told there are multiple contracts coming in on the property. Now that you know the numbers, you must decide how much you wants this property. Should you consider putting in a contract above list price?

A $65,000 bid would likely reflect a $30,000 net profit margin. Offering above list price would change the profit to something under $25,000. Remember, you have the listing agent in your corner so this will give you leverage in this situation too.

You make the decision to go $2,000 over list price to stack the odds of getting the property in your favor. In this case, you are acting as a smart investor. You will still be looking to make a profit of $23,000. This will accomplish your goal if the contract is accepted.

Wouldn’t it be nice to have a crystal ball and know the exact figure of all other contracts competing with you? Unfortunately, we don’t and we need to rely on our gut instinct, and all available resources to make a determination.

It is difficult to know exactly where your bid should be placed even if you are an expert in the market. If you are working with a listing agent, they may be able to offer you clues.

It depends on the state law but some agents may be able to disclose the price of the other offers. There is a fine line when discussing this with an agent but there is not a national law that prohibits this. However, an agent may be bound by a confidentiality agreement or the law by the state. Check the state you reside in for clarity.

Disclosure & Compliance Note: The links above redirect to the website of Buyrego Realty, LLC, an Illinois licensed real estate brokerage where Jeff Knize is the Designated Managing Broker. The use of the “Home Value Estimator” is for marketing purposes and general information only and does not constitute a formal USPAP appraisal of real property.